Nitrogen at the Chokepoint: How APAC Agri-Food Will Navigate the Hormuz Crisis

Why this matters now

Why this matters now

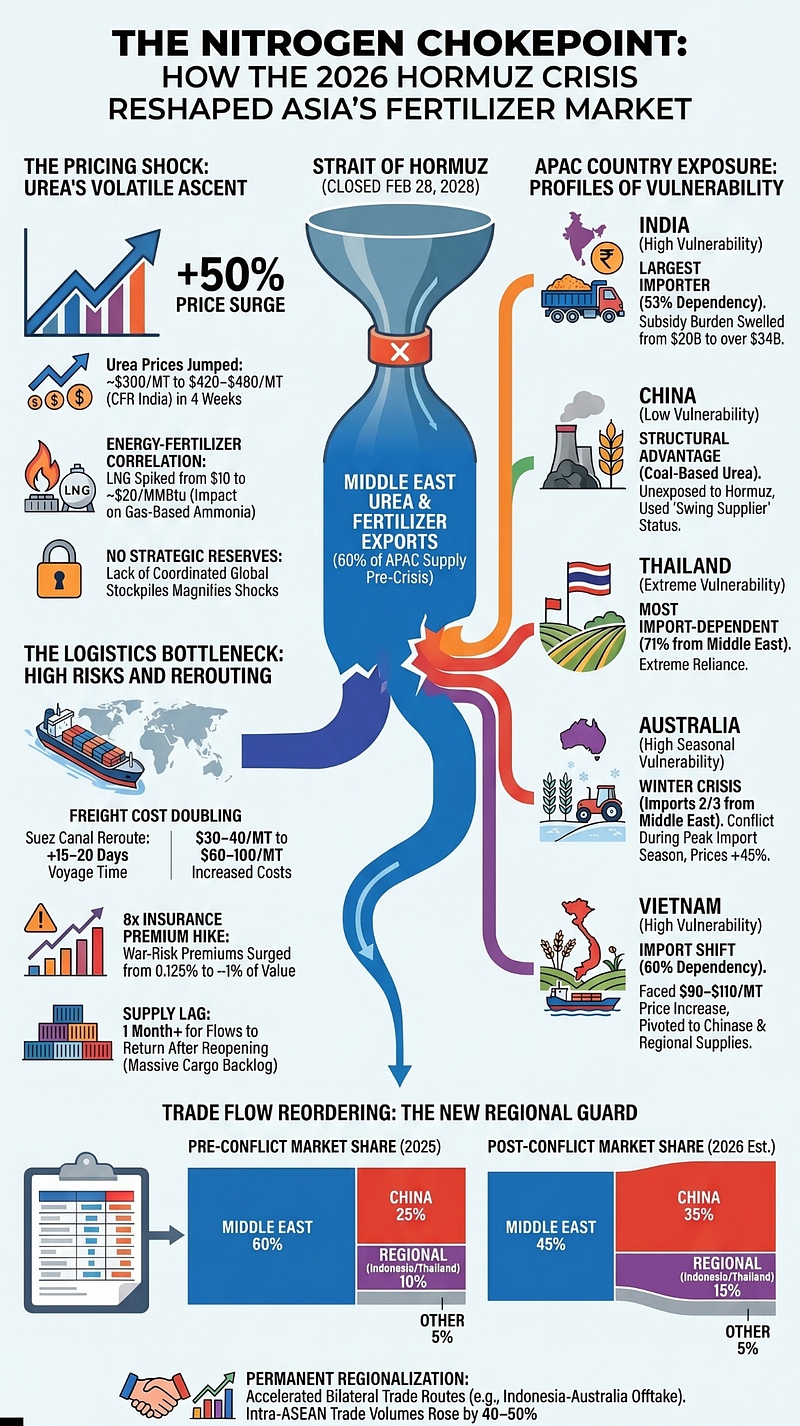

On February 28, 2026, the initiation of Operation Epic Fury and the subsequent conflict severely restricted commercial shipping through the Strait of Hormuz. This narrow waterway is the world’s most critical energy and agricultural chokepoint, traditionally handling approximately 20% of global liquefied natural gas (LNG) and up to 35% of globally traded urea. As an investor monitoring cross-border agri-food systems, it is clear that what began as a Middle Eastern energy shock has rapidly metastasized into a structural agricultural crisis. We are no longer just pricing in oil volatility; we are pricing in the core caloric input for the Asia Pacific region. The U.S. implemented a naval blockade targeting Iranian ports on April 12, 2026, but the actual enforcement and the duration of this maritime paralysis remain highly fluid and unpredictable.

Current APAC nitrogen market state

The Asia Pacific region consumes roughly 60% of global nitrogen fertilizers but relies on imports to meet approximately 65% of its urea demand. Pre-conflict, Middle East FOB urea prices sat between $265–$300/MT. By mid-April 2026, following the outbreak of war, granular urea from Southeast Asian producers (like Brunei) was selling at approximately $710/MT FOB. Simultaneously, China — the region’s natural swing supplier — has heavily restricted its urea and phosphate exports to protect domestic food security, a policy expected to last until at least August 2026. APAC is caught in a vice. The region’s structural deficit is colliding with a historic supply shock, transferring pricing power entirely to remaining regional producers like Indonesia. Relying on the spot market in this environment is a margin-destroying proposition for downstream agribusinesses.

Conflict transmission channels

The geopolitical shock is transmitting to the farm gate via three distinct channels:

- Energy Feedstock Spikes: Natural gas (LNG) is the primary feedstock for ammonia and urea. The conflict has damaged key infrastructure, heavily inflating production costs for Middle Eastern plants.

- Maritime Logistics Paralysis: War-risk insurance premiums surged up to tenfold (reaching 1.5% of hull value), forcing major carriers to reroute via the Cape of Good Hope — adding 10 to 14 days and roughly $500,000 per voyage.

- Physical Supply Bifurcation: The market isn’t facing a 100% embargo. Maritime intelligence shows dozens of vessels still transiting by spoofing AIS data. Access is now determined by a willingness to pay ruinous insurance premiums or engage in deceptive shipping practices.

Country exposure in APAC

Vulnerability across APAC is starkly asymmetrical. India, heavily dependent on the Middle East for about 40% of its urea, has opted to absorb the shock via its sovereign balance sheet, raising the Nutrient Based Subsidy (NBS) by 10% for the upcoming kharif season. While this shields the Indian farmer temporarily, it places massive strain on government fiscal targets, with the subsidy bill projected to balloon by billions of dollars.

Conversely, import-dependent Southeast Asian nations lack this fiscal buffer. Thailand sources 71% of its urea imports from the Middle East. Australia, entering its peak winter demand season, has seen local urea prices spike 45% to A$1,200/t as it scrambles to replace Middle Eastern cargoes with limited Southeast Asian supply. For price-taking markets like Vietnam and the Philippines, it is highly uncertain whether farmers can absorb these costs or if we will see immediate demand destruction — where farmers reduce application rates, inevitably triggering yield losses and regional food inflation by Q3/Q4 2026.

Scenarios

- Base Case (Prolonged Disruption): Operating under the assumption that the Strait remains contested through 2026, Middle East exports to APAC will stabilize at roughly half their normal volume. Red Sea ports (like Yanbu and Jizan) and Oman’s Duqm port are currently being utilized to bypass Hormuz, but this pipeline and alternative port infrastructure can only handle a fraction of the region’s normal throughput. Prices will remain elevated, and logistics premiums will become the new normal.

- Stress Case (Severe Escalation): Direct, sustained damage to Saudi or Qatari production infrastructure could collapse Middle East output by 80–90%. This would drive CFR India/SE Asia prices past peak 2022 levels, causing acute physical rationing across APAC.

- Downside Price Risk (Rapid De-escalation or Chinese Re-entry): If China abruptly repeals its export ban before August 2026 to capture record high prices, millions of tons of urea could flood the market. This is the primary bearish risk for anyone holding long inventory positions today.

Strategic implications

For operators and procurement teams, the era of relying on just-in-time, lowest-cost procurement from the Persian Gulf is effectively over. Supply chain certainty now outright dictates survival over unit cost. To navigate this, agribusinesses need to execute defensively on three fronts:

- Prioritize Physical Supply Over Spot Pricing: Abandon the strategy of holding out for spot market corrections. Procurement teams must prioritize securing volume — even at a premium — from geographically secure, regional producers (like Indonesia or Malaysia) to guarantee supply for the upcoming planting windows. We are already seeing this pivot at the national level, with Australia aggressively seeking long-term offtakes with Indonesian producers to secure geographic proximity.

- Defend Working Capital: The jump from $300/MT to $710/MT FOB doesn’t just erode margins; it severely drains liquidity. Procuring the same physical volume of fertilizer now requires more than double the capital. Operators must proactively engage lenders to expand credit facilities and lock in financing early, before regional lending conditions tighten in response to the broader macro environment.

- Accelerate Bio-Input Integration: Hedging against physical nitrogen shortages means rethinking the input stack. Similar to the surge in biologicals seen in Brazil following the 2022 supply shock, APAC operators should accelerate the integration of bio-inputs and nitrogen-fixing alternatives. What was previously viewed as a long-term sustainability mandate is now a critical, immediate tool for blending down overall application costs and protecting yields.

30/90-day watchlist

We should monitor three leading indicators over the next quarter:

- Chinese Export Quotas: Any policy shift in Beijing ahead of August 2026 will immediately dictate the APAC price ceiling.

- Maritime Evasion Volumes: Monitoring the flow of “dark” transits via intelligence providers will indicate the true physical liquidity of the market versus the “official” halted commercial volumes

- Crop-to-Fertilizer Exchange Ratios: Nominal prices only tell half the story; farmer purchasing power dictates actual demand. Watch these three benchmarks to anticipate acreage shifts and application cuts

- Corn-to-Urea (e.g., CBOT Corn vs. ME FOB Urea): This ratio recently spiked from 75 to 126 bushels per ton in the U.S. Sustained highs signal imminent demand destruction, forcing farmers to slash nitrogen rates or switch to less intensive crops like soy.

- Soy-to-MAP: Brazilian ratios hit the top of their five-year range in April 2026. With farmers already lagging behind historical procurement schedules, this is the primary bellwether for sudden phosphate demand strikes.

- The Potash (KCl) Divergence: Unlike nitrogen and phosphate, potash exchange ratios remain below five-year averages. This divergence highlights where farmers are most likely to reallocate their constrained working capital to salvage yields.

Update: 1 May 2026 - Created Dashboard to monitor these signals here: https://apac-fert-monitor.vercel.app/#/

What could invalidate this view

Any single one of the following three catalysts occurring in isolation is sufficient to materially weaken or entirely invalidate the projection of sustained high prices in APAC:

- A Solo Chinese Policy Reversal (The Primary Bearish Risk): China has withheld urea and phosphate exports to protect domestic food security, a policy expected to last until August 2026. However, if Beijing reassesses its stockpiles and repeals the ban early, its return as the region’s natural swing supplier would independently crash the APAC spot market. This action alone would trigger rapid global price declines, heavily punishing any operator holding long inventory positions.

- Accelerated Return of Iranian Export Volumes: Iran is the world’s third-largest urea exporter, and its production is reportedly returning to full rates. While the U.S. blockade complicates standard shipping, maritime intelligence confirms successful blockade breaches via “dark fleet” tankers. If Iranian output successfully utilizes these illicit or grey-market channels to reach APAC buyers at scale, it would independently loosen regional supply balances and pull CFR prices down, regardless of official commercial shipping status.

- A Sustained Ceasefire and Insurance Normalization: An initial two-week ceasefire was announced on April 8, 2026, but marine insurers require a “stable and verifiable” peace before reducing current ruinous war-risk premiums (which sit around 1% of hull value). If this diplomatic breakthrough holds and insurers return to the market, it independently resolves the logistics paralysis. Eliminating the freight premiums associated with Cape of Good Hope rerouting would substantially drop the price floor for delivered nitrogen in APAC.

Sources

- “2026 Strait of Hormuz crisis — Wikipedia,” Wikipedia, April 17, 2026.

- “Chokepoint: How the War with Iran Threatens Global Food Security,” Center for Strategic and International Studies (CSIS), March 11, 2026.

- “Strait of Hormuz Live Tracker — Shipping Disruption Dashboard,” HormuzTracker, April 14, 2026.

- “Southeast Asian granular urea sold at around $710/t fob,” Argus Media, March 13, 2026.

- “China and Iran Redraw Fertilizer Trade Lines,” StoneX, February 17, 2026.

- “Strait of Hormuz Live Tracker — Carrier Status & Reroute Cost Calculator,” HormuzTracker, April 14, 2026.

- “Monitoring the Strait of Hormuz: Real-Time Maritime Risk & Transit Data,” SeaVantage, March 27, 2026.

- “April 15, 2026: Iran War Maritime Intelligence Daily,” Windward, April 15, 2026.

- “UPDATE 1-India raises fertiliser subsidy as US-Iran war lifts global prices,” Sahm Capital, April 8, 2026.

- “Indian government raises NBS for N, P, S,” Argus Media, April 8, 2026.

- “Prices of Asia-Pacific’s fertilisers, petrochemicals set to surge on Iran war: ADB,” Eco-Business, March 30, 2026.

- “Red Sea ports now central to Middle East sulphur supply,” Argus Media, April 17, 2026.

- “What Are the Effects of the Iran War on Agriculture?”, Inter-American Dialogue, April 9, 2026.

- “The Iran Conflict and Fertilizer Markets: Why Brazil Faces Greater Near-Term Risk than the U.S.,” farmdoc daily (University of Illinois), April 10, 2026.

The views expressed are the author’s own and do not reflect the views of any associated organizations.